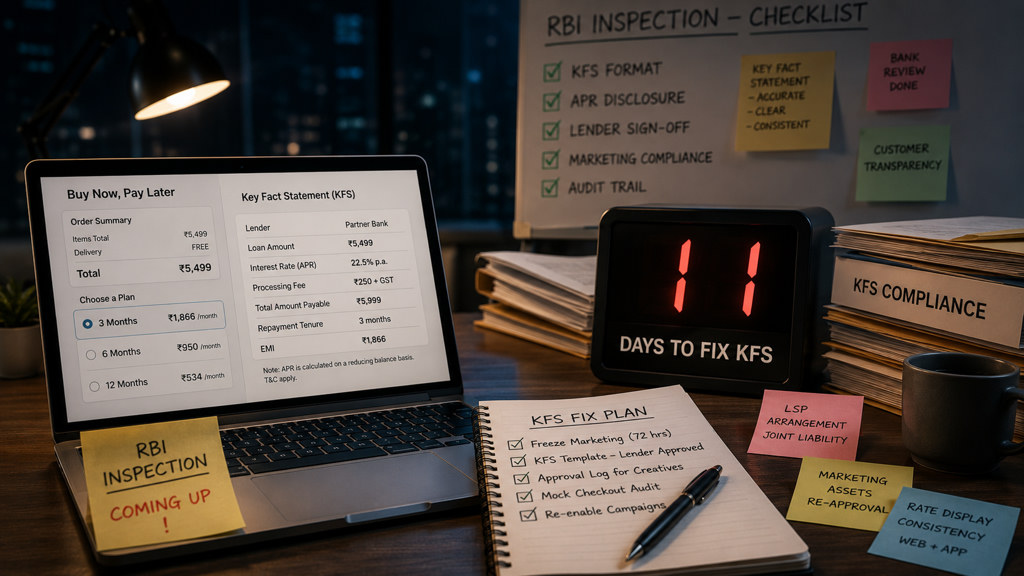

We had 11 days to fix KFS before RBI asked questions

Founder Voices · Series B BNPL platform (anonymised) · Series B · 2M+ monthly active users

The problem

The founder’s checkout BNPL widget showed a summary page that investors loved in demos — but it did not match the Key Fact Statement format RBI expects on merchant checkouts. A partner bank flagged mismatched APR display two weeks before a scheduled RBI-themed inspection of the LSP arrangement.

In conversation

“We did not need a lecture on the KFS rules. We needed a ordered list of what to change in the widget, what to log for the bank, and what to pause in performance marketing until legal signed off.”

— Founder & CEO, BNPL platform

“The surprise was marketing — every influencer creative had to be re-approved because the bank’s name appeared next to a rate footnote we had never standardised.”

— Founder & CEO, BNPL platform

What we told them to do

- Freeze new marketing creatives for 72 hours and inventory every live asset mentioning credit or EMI

- Ship a single KFS template approved by the lender — same fields, same order, same APR basis on web and app

- Add an internal approval log: lender sign-off timestamp per creative batch

- Run a mock checkout audit with the bank’s compliance team before re-enabling paid campaigns

What other founders can take away

- KFS is a product surface, not a PDF your legal team files away

- LSP arrangements make marketing jointly liable — treat creatives like regulated copy

- Build a ‘regulatory diff’ ritual before every major sale or inspection season

Note: Published with the founder’s consent. This is not legal advice and does not create a lawyer-client relationship.

This publication is for general information only and does not constitute legal advice. Regulatory positions evolve; verify current notifications and obtain counsel before acting. © 2026 SB Tech Associates.